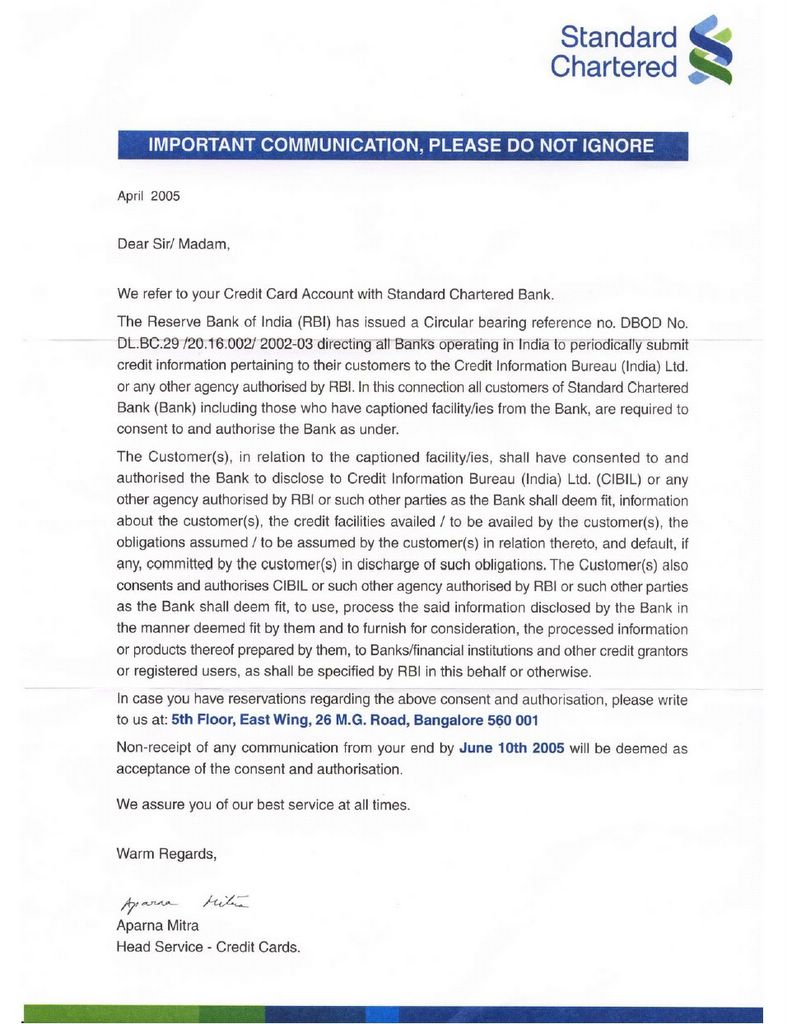

Ms Aparna Mitra (Head Service – Credit Cards) of Standard Chartered Bank has sent a letter to the cardholders of the bank requiring consent from the customers (actually, not as much as requiring as intimating the assumption of consent – the letter states “Non-receipt of any communication from your end by June 10th 2005 will be deemed as acceptance of consent and authorization”) in respect to sharing customer information with other parties.

Ms Aparna Mitra (Head Service – Credit Cards) of Standard Chartered Bank has sent a letter to the cardholders of the bank requiring consent from the customers (actually, not as much as requiring as intimating the assumption of consent – the letter states “Non-receipt of any communication from your end by June 10th 2005 will be deemed as acceptance of consent and authorization”) in respect to sharing customer information with other parties.The letter is made out as being occasioned by a (3-year old) circular from the Reserve Bank of India “bearing reference no. DBOD No. DL.BC.29/ 20.16.002/ 2002-03 directing all Banks operating in India to periodically submit credit information pertaining to their customers to the Credit Information Bureau (India) Ltd. or any other agency authorized by RBI”

In a classic sleight-of-hand, the letter then goes on to construct a clause for consent and authorization that goes much beyond what the RBI requires and where any future extension of consent and authorization will be beyond what is required by an independent body such as the RBI.

According to the clause which all customers are required to agree:

“authorize the Bank to disclose to Credit Information Bureau (India) Ltd. (CIBIL) or any other agency authorized by RBI or such other parties as the Bank shall deem fit” (note that “the Bank” is Standard Chartered); “The Customer(s) also consent and authorizes CIBIL or any such other agency authorized by RBI or such parties as the Bank shall deem fit, to use, process the said information disclosed by the Bank in the manner deemed fit by them and to furnish for consideration, the processed information or products thereof prepared by them, to Banks/ financial institutions and other credit grantors or registered users, as shall be specified by RBI in this behalf or otherwise” (Emphasis provided)

In one stroke, Standard Chartered is not just assuming full ownership of all information that customers have submitted but is also abrogating the right to provide it – free or otherwise – to anyone it pleases, for any purpose that Standard Chartered or the subsequent entity (in whose hands this information reaches) may want to use it for.

And Standard Chartered is doing this beautifully – by just appending a few words to what the RBI is requiring it to do (for the record, the creation of CIBIL and RBI’s support to this new organization in form of requiring banks to share data with CIBIL is an extremely important and beneficial step for all involved in the personal credit industry – including customers – in our country).

Why is this important at all? Well, as an overarching cause, note that they’re taking your and my personal particulars (including, but not just restricted to, financial data) and trading in it – which is absolutely not their remit. And, to be very specific, note that the next time an auto-loan salesperson calls you on your mobile phone, you have actually authorized that call to be made.

No wonder there are a number of people who despise these MNCs (in banking or otherwise): Standard Chartered wouldn’t have tried such a trick in any developed market that it operates in – it is using the lower standards (with respect to data protection and consumer awareness) prevalent in this country to “get away with what it can”. Despicable. Next, consider that it is such exploitation of loopholes that lead to the government and regulatory agencies becoming very prescriptive in their recommendations – so, the RBI could have had issued a circular with specific wording on the communication between banks and their customers. But, had that been the case, I am sure there would be editorials and (planted?) news stories about “license-raj-mentality” or “overzealous regulators” and such like.

For things to change (without throwing out the baby with the bathwater), at least one of the three conditions – consumers becoming powerful as an organized group, RBI’s ombudsman becoming proactive and powerful, some sort of a producers guild becoming forward looking in respect to consumer issues – need to be met. Till then, thank you very much but I do not want any personal loans, so don't call me: should my needs change, I will call you.

N.b.

I have written to Ms Mitra at the address supplied, specifically excluding the discretionary portions from the consent, but I doubt if she or her employer will pay any heed (surprise me, StanChart).

13 comments:

Hi

Thanks for bringing these amazing tricks to my notice. I hope it is okay with you if I post this on my website with a link to your blog.

Sucheta Dalal

www.suchetadalal.com

Right on, Ojha Sahib. I would not be surprised if they don't receive a single response to their 'respond by so and so date' mailer and go on to assume its perfectly kosher to sell our personal information to call centre monkeys.

In the developed world, fear of a class action suit or a PIL from someone like you would be enough to keep them from trying a low trick like this, but bhai, since its India, where we are forced to live out large parts of our lives in public anyway, why would a little less privacy hurt?

Do keep us posted on what happens.

Mahesh Jayaraman

No wonder Citi beats the daylights out of StanChart.

Citi effected this trick more than a year ago. I tried speaking to somebody who could answer my concerns and all I could do was get to speak to a CSA who is unsure of the direction in which the sun sets.

My solution: moved my business away from Citi

True. Dare any bank to send this communication to an 'American' ( Read US) customer , and you have invited yourself a suit for a Million Dollars ( or More!) .

The Standard Chartereds of the world can take us for a ride as long as basic human values take a backseat in this country.

My thanks to Ms Dalal for bringing this matter to my attention through her columns in the Indian Express.

I would like to state that Standard Chartered offers a great entertainment service for us native Indians and provides job opportunities for BPOs that would languish otherwise in unemployment.

Let me give you a real-life example from their tele-banking service, because it is not nice to knock their credit cards in isolation.

My wife called Standard Chartered last week to ask about a SWIFT transfer from Switzerland. She was taken back when told that there was no credit from Switzerland, but one from China instead! "Some 80 CHF Maam" the poor sod insisted, when my wife dared to say that we were not expecting money from China.

My Australian mobile provider would charge me good money for a joke of this genre on 123!

Hey,

They've made a good use of the legal language to delude the public. Yeah, but, we are not the only ones to feel cheated.

Have a look at http://householdwatch.com to see how the "American" (read U.S.) public is cheated using much more sophisticated tricks.

Happy browsing,

Mayank.

Dear Sir,

Thanks for the eye opener, and thanks Ms. Dalal. But I wonder, are there ANY banks who are immune to this practice. Can any bank stand up and say we do not do this. I wonder, what methods the others have devised. They won't be far behind in this game.

Thanks

Dear Mr. Ojha,

Re the Stachart CIBIL consent scam, may I respectfully request you to visit my own blog in the matter and I am already in court on this issue, and surprise-surprise (!) STANCHART advocates have run away from the court now since all their skeletons have come tumbling out. Incidentally it was my hacking complaint which suddenly energised RBI and FinMin to pass the CIBIL Act after so many years.

I wud appreciate yr. specialised inputs in this matter.

Sarbajit Roy

my blog url is:

http://sarbajit-roy.blogspot.com

One need not live in the developed world to fight this kind of nonsense. The time-tested common law of contracts (to which the United States and India both are inheritors) bars the use of silence as a means of accepting any offer -- unless the offeree (in this case, Mr. Ojha) has himself agreed that silence shall indicate acceptance, or unless the government has by statute empowered Standard Chartered to construe silence as acceptance. Neither has happened here.

Granted, the U.S. provides greater consumer protections by statute than does India, but there is no such thing as public-interest litigtion here (indeed it is barred by the courts), and no class action lawsuit is required. One harmed individual could sue under contract law that there was no agreement between him and Standard Chartered to this effect to begin with -- and that could set precedent, at least in his jurisdiction. At a more advanced stage, one might even put forth the bolder claim of a violation of his due process rights (e.g., state action without reasonable notice -- but I won't get into that here).

To my mind, this has little to do with the evils of MNCs or with discrimination against people living in poorer nations. Large corporations will try to get away with whatever they can whenever they can -- Enron is a case in point -- and India's judicial and administrative institutions are certainly not those of a banana republic. MNCs are indispensable to modern life, but require effective oversight by governments and publics (blogging activity such as this certainly helps). That's hard work, but necessary for every nation on earth, rich or poor, and no reason for India to sour on MNCs!

With this googly, SCB now topples ICICI and Citibank from the Worst Bank in India position.

I sent SCB the following letter in response to their oh-so-clever communciation.

Sravana B Varma

Manhattan Hub

Unity Building

2, Mission road

Bangalore 560002.

Sub: Authorization to SCB to share customer information.

Dear Mr. / Ms. Sravana Varma,

I received a communication with my previous statement from your credit card company which refers to RBI Circular No. DBOD No. DL.BC.29/20.16.002/2002-03.

According to your communication, the above-mentioned RBI circular requires that all banks including Standard Chartered Bank (SCB) to periodically submit:

1. credit information pertaining to customers

to

1. Credit Information Bureau (India) Ltd. (CIBIL), or

2. Any other agency authorized by RBI.

However, I note that the authorization following the above in the same communication effectively allows you to share:

1. information about the customer,

2. credit facilities availed by the customer,

3. credit facilities available to the customer,

4. obligations assumed / to be assumed by customer in relation to the above and

5. defaults information

to

1. Credit Information Bureau (India) Ltd. (CIBIL), or

2. Any other agency authorized by RBI,

3. Any party as the Bank (SCB) may deem fit.

Further, in a distinct departure to the easy-going language of all your other communications, this “important communication” is full of legalese. I also note that the said RBI circular is more than 3 years old.

To me this seems to be a classic example of unethical business practice wherein you have attempted to gain authorization for more than what is legally required (all items that I have italicized) by shrouding the message in legalese. Whereas I may / may not pursue the issue of unethical business practice separately, I certainly do not authorize you to share any information with anyone (CIBIL or other RBI authorized entities) without clarifying the circular in detail to me in written to my satisfaction.

Non-receipt of any communication from your end by July 1st, 2005 will be deemed as acknowledgement of my notification of non-consent and non-authorization and of your consent to send me your written clarification by 8th July 05, on the non-receipt of which I shall seriously consider pursuing the issue of unethical business practice at the appropriate forums.

Regards,

Tilak Nag

It is totally unethical. It is unfortunate that RBI is a party to this unethical practice. A friend of mine applied for a car loan to a nationalized bank. it was rejected as in CIBIL credit report it was found that Standard Chartered has shared information about late payment of a credit card bill and this was treated as a negative point. The fact is that the S&C bank was at default as it has sent the bill after due date and when my friend pointed it out then S&C Bank accepted their mistake and apologized but shared the incomplete information to CIBIL. This they did to harass my friend and he did not even know about it.

Post a Comment